Key findings:

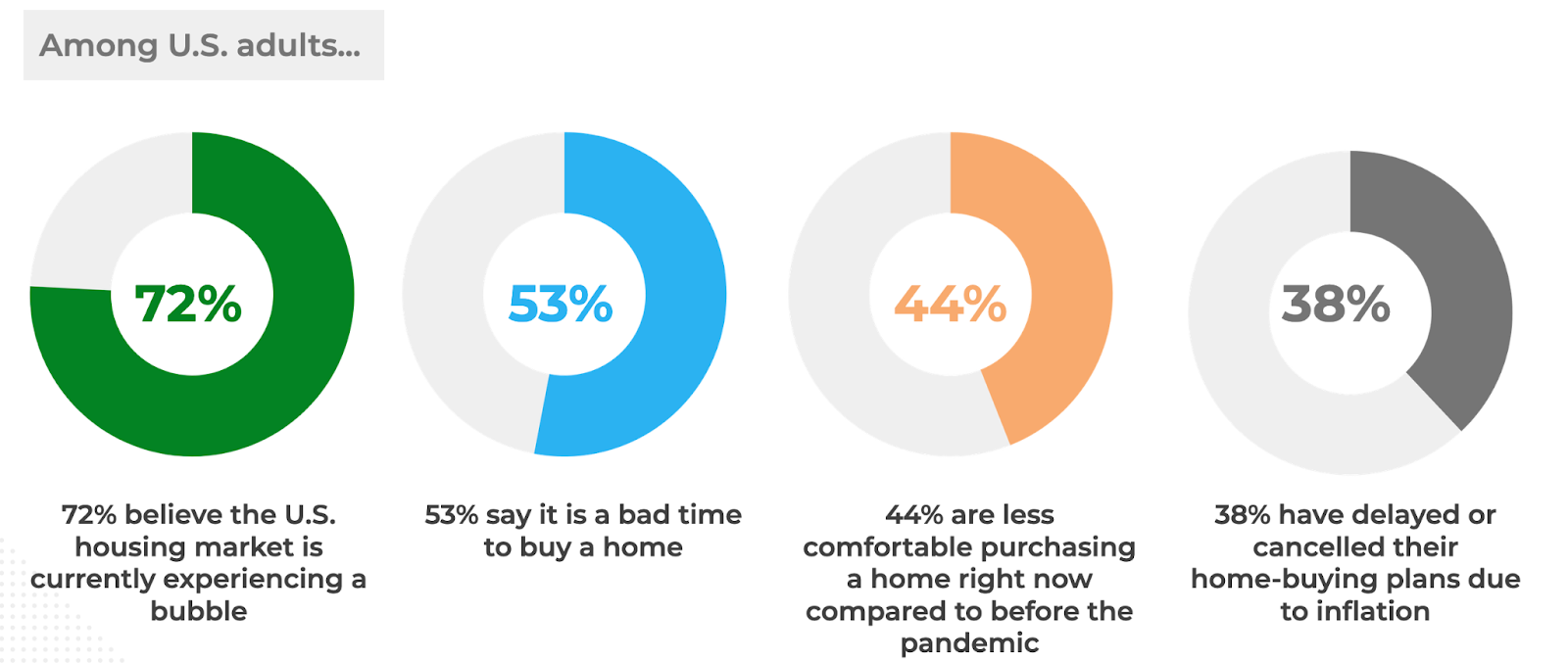

- Concerns over affordability overwhelm homebuyers, as nearly 3 in 4 (72%) of U.S. adults believe the housing market is experiencing a bubble

- Millennials are the fastest growing group of homebuyers, with nearly 1 in 5 looking to purchase a home now or within the next year

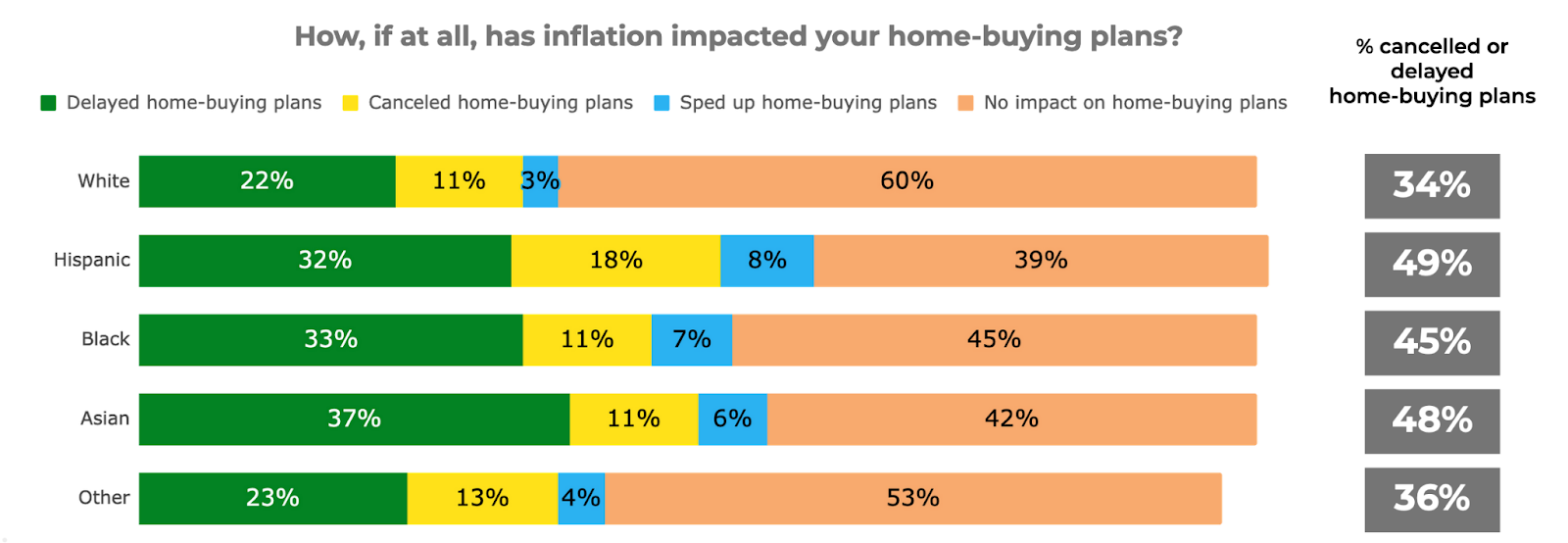

- Hispanic, Black, and Asian Americans’ home-buying plans are disproportionately impacted by rising prices, compared to white Americans

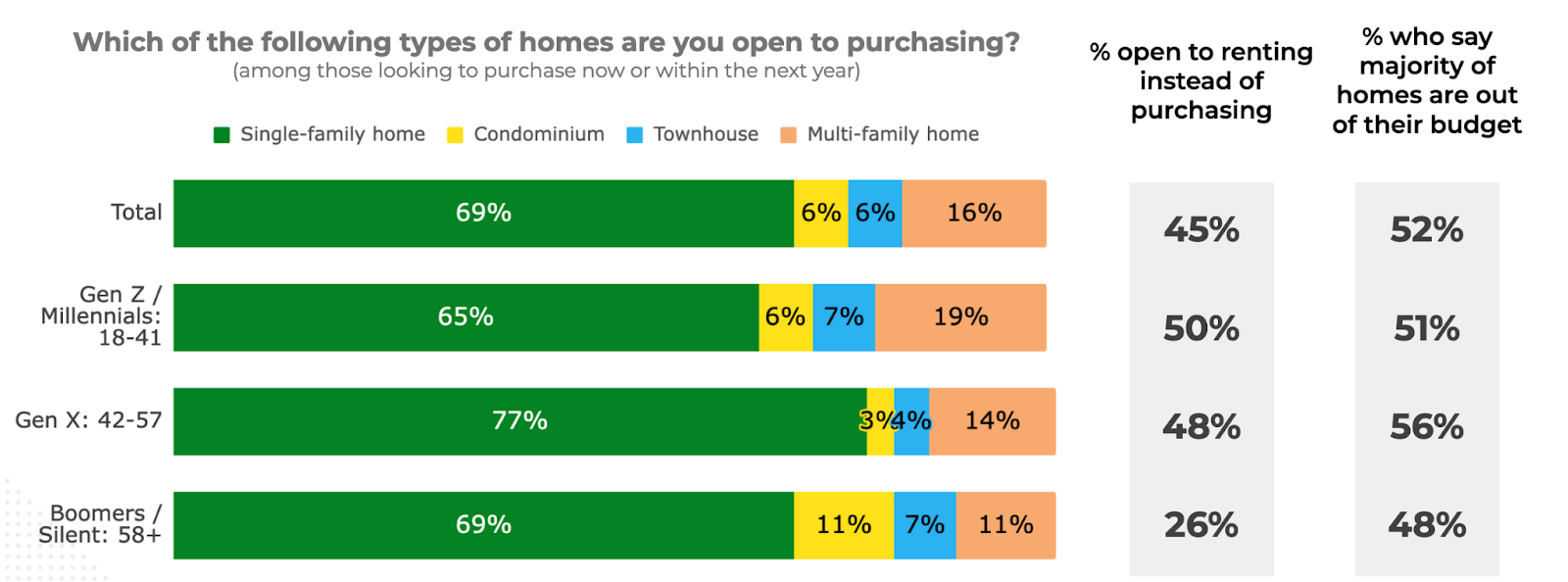

- Gen Z and Millennial homebuyers express greater interest in multi-family homes and rental properties

- Online mortgage lenders’ lower credit rating requirements are a main draw for younger and lower income borrowers

Concerns over affordability overwhelm homebuyers, as nearly 3 in 4 (72%) of U.S. adults believe the housing market is experiencing a bubble

Rising home prices are leading to widespread uncertainty in the housing market, as concerns over affordability dim prospects of homeownership. Nearly 3 in 4 (72%) of U.S. adults believe that the U.S. is currently experiencing a housing bubble, a sentiment shared across urban (74%), suburban (73%), and rural areas (70%). Over half (53%) say it is currently a bad time to buy a home. Inflation and other economic shocks from the last few years have impacted home-buying plans: 44% are less comfortable purchasing a home now compared to before the pandemic, and 4 in 10 (38%) have delayed or canceled their home-buying plans due to inflation.

Millennials are the fastest growing group of homebuyers, with nearly 1 in 5 are looking to purchase a home within the next year

Aspirations for homeownership are highest among Millennials, as the generational cohort made up the largest group of homebuyers from 2020 or later (36% vs. 26% for Gen X and Boomers). They also remain most active in the current housing market, with 17% currently looking to purchase a home or plan on purchasing one within the next year, compared to 12% of Gen Zers and Gen Xers.

Hispanic, Black, and Asian Americans’ home-buying plans are disproportionately impacted by rising prices, compared to white Americans

Recent inflation has disportionately impacted Americans of color, with non-white Americans are nearly 1.5 times more likely than white Americans to have canceled or delayed their home-purchasing decisions due to increasing housing prices. Roughly 1 in 3 (34%) of white Americans have delayed (22%) or canceled (11%) their home-buying plans, while:

- 49% of Hispanics have canceled (18%) or delayed (32%) their home-buying plans

- 45% of Blacks have canceled (11%) or delayed (33%) their home-buying plans

- 48% of Asians have canceled (11%) or delayed (37%) their home-buying plans

Gen Z and Millennial homebuyers express greater interest in multi-family homes and rental properties

Aspiring homeowners still vastly prefer single-family homes (69%) over condominiums (6%), townhouses (6%), or multi-family homes (16%). Gen Z and Millennial homebuyers, while still preferring single-family homes over all other types of properties, are more likely than older generations to be open to purchasing multi-family homes.

1 in 5 (19%) of Gen Zers and Millennials looking to purchase a home now or within the next year would consider a multi-family home, compared to 14% of Gen Xers and 11% of Boomers and those of the Silent Generation.

Willingness to rent instead of buying a home is also a growing alternative for homebuyers - 50% of Gen Z and Millennials looking for a home are open to renting instead of purchasing, with a similar percentage of Gen X homebuyers also leaving the door open.

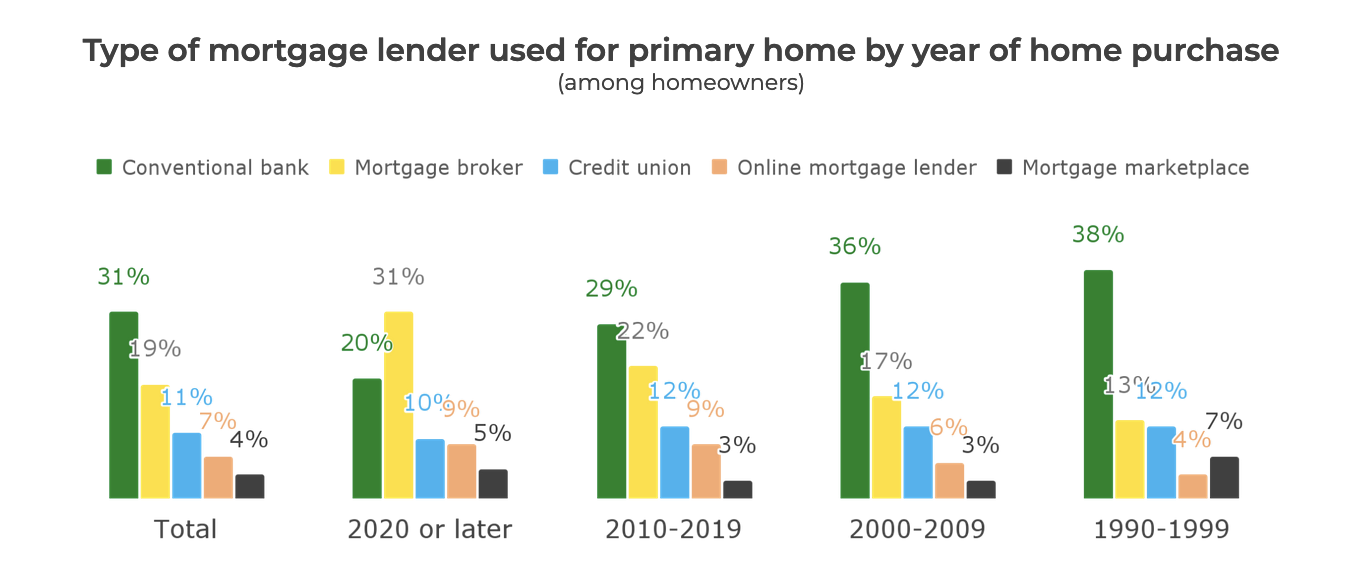

Newer homebuyers turn to mortgage brokers at the expense of conventional banks

Newer home buyers are opting to get a mortgage through a mortgage broker instead of through a conventional bank. Mortgage brokers made up 31% of mortgages from homes purchased in 2020 or later, compared with only 20% of conventional banks. Comparatively, mortgages through conventional banks are most popular for homes purchased in 2019 or earlier. Credit unions, online mortgage lenders, and mortgage marketplaces still remain among the minority, even among more recent home purchases.

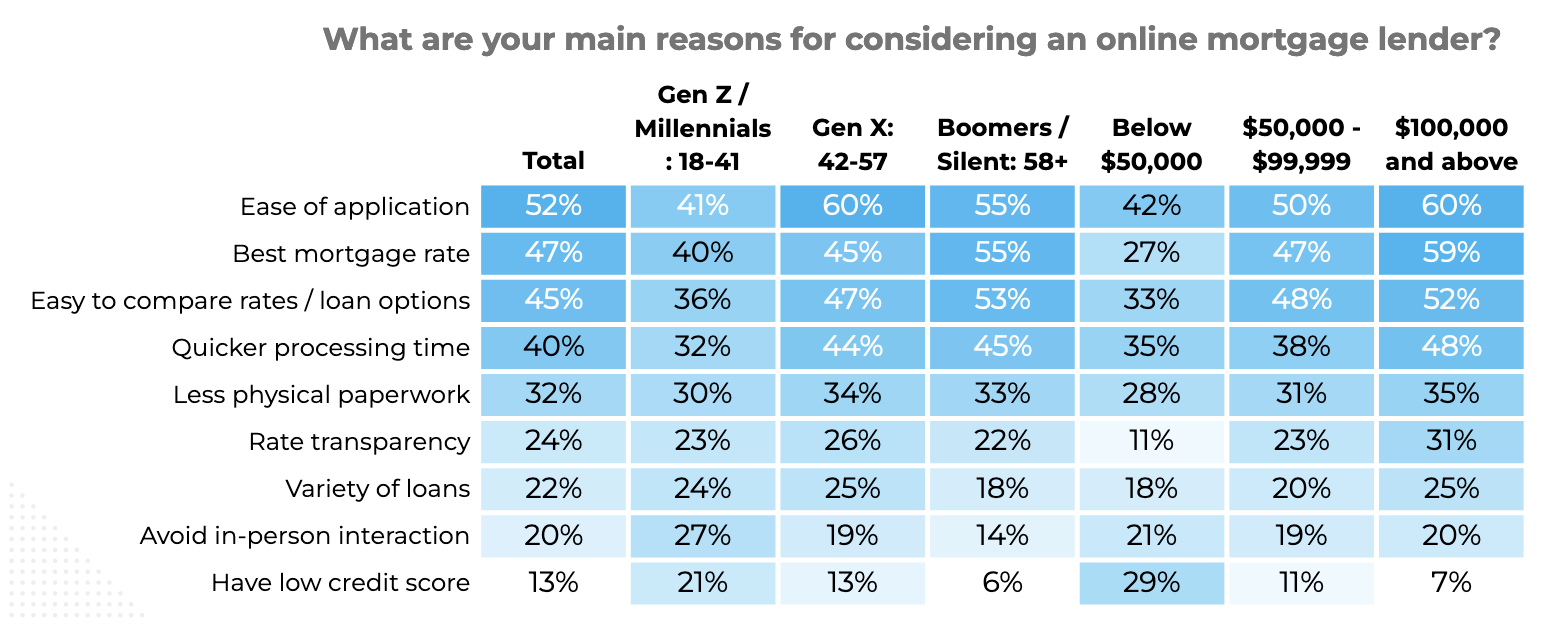

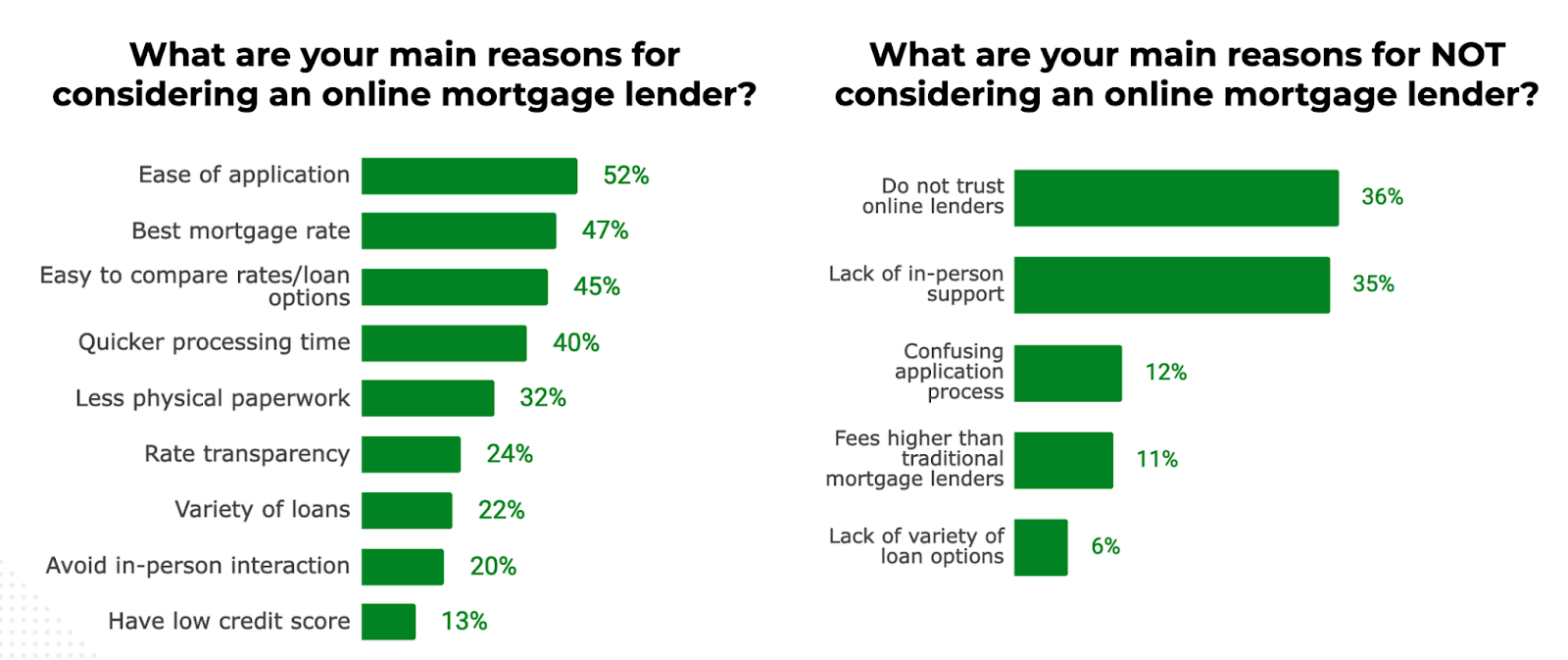

Online mortgage lenders’ lower credit rating requirements are a main draw for younger and lower income borrowers

Ease of navigation, lower mortgage rates, and comparison tools are the leading drivers of consideration for online mortgage lenders. Lower credit requirements are among the main draw for lower-income borrowers as they seek alternative financing apart from conventional banks. Younger age cohorts, especially Gen Z and Millennials, are also more likely to consider online mortgage lenders due to lower credit scores, but also prefer to not having to interact with a person during the application process.

Despite the advantages offered by online lenders, general distrust and a lack of in-person support remain hurdles for adoption. Among current homeowners and homebuyers who did not consider an online mortgage lender, 36% cite a general distrust toward online lenders, and 35% a lack of in-person support as their main reasons for avoiding them.

Read more about our polling methodology here.